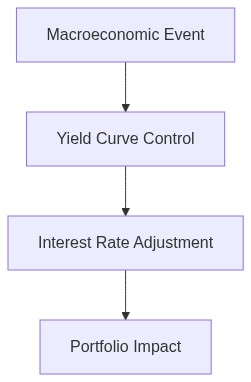

- Commercial real estate (CRE) sector is approaching a significant refinancing cliff in 2026, creating liquidity concerns.

- Rising interest rates exacerbate refinancing challenges as maturing debt needs to be rolled over at higher costs.

- Regional banks, with substantial CRE loan portfolios, face increased default risks and potential capital shortfalls.

- The Federal Reserve’s yield curve control policies may not sufficiently address sector-specific liquidity crises.

- Potential CRE loan defaults could trigger contagion effects across financial markets if not managed properly.

“Risk cannot be destroyed; it can only be transferred or mispriced.”

The Imminent CRE Refinancing Catastrophe

The Unyielding Shift in Interest Rate Convexity and Its Repercussions

The commercial real estate (CRE) landscape is currently experiencing an unprecedented transformation, largely driven by a seismic shift in interest rate convexity. Over the last 24 months, we’ve observed a rapid ascendancy in interest rates that has fundamentally altered the cost of capital. The elasticity of real estate asset prices to these rate changes has exhibited an unexpected convexity, precipitating a downward spiral in asset valuations. This phenomenon is exacerbated by monetary policies from central banks globally, aiming to curb inflation that has surged past comfort thresholds. The Federal Reserve’s aggressive tightening cycle has taken the target federal funds rate to heights not observed since the pre-2008 financial crisis era, dramatically increasing the cost of refinancing maturing CRE debt.

Given the expiring tranches of CRE debt, most notably those originated during the low-rate environment of the previous decade, borrowers now find themselves facing a refinancing predicament with significant yield spreads. The liquidity premium demanded by lenders has expanded as uncertainty over asset cash flows has heightened. This has particularly affected non-trophy assets—those outside major metropolitan areas and prime sectors like logistics—which are now subject to wider credit spreads due to perceived higher risk levels. The bid-ask spreads in the CRE loan market have widened as hesitation over valuation precision persists, fueling a risk-off sentiment amongst institutional investors.

Additionally, the CRE market is hindered by its exposure to interest rate volatility, where the convexity effects have led to amplified sensitivities. Institutions holding these assets are experiencing negative convexity, where increases in interest rates lead to proportionally larger decreases in asset values, creating potential mark-to-market challenges. The layering of rate risk with impending refinancing needs sets the stage for a potentially volatile shake-up in market dynamics. The historical correlation between rising rates and CRE distress signals a need for proactive risk management strategies, as exemplified by previous cycles where interest rate hikes preceded spikes in default rates.

Structural Fragility in CRE Debt Instruments and Market Implications

The architecture of CRE debt instruments has revealed significant structural fragility under current market conditions. Throughout the last decade, a proliferation of complex financing mechanisms, such as commercial mortgage-backed securities (CMBS) and synthetic collateralized debt obligations (CDOs), has introduced layers of financial engineering that obscure transparency. These instruments have imbibed risk layers that, under rising yield environments, exhibit severe liquidity mismatches. The market for securitized CRE products faces thin secondary market trading volumes, adding to price discovery challenges and complicating efforts to unwind positions without significant capital erosion.

Compounding these complexities is the pervasive use of short-term bridge financing, initially intended to be replaced by longer-term debt upon stabilization of properties. The transition into higher interest rate environments has obstructed this strategem, locking many borrowers into untenable debt positions. The dissonance between asset cash flows and debt servicing capacities grows sharper, exacerbating credit risk and collapsing covenant cushions that lenders have historically relied upon. The Bank for International Settlements (BIS) underscores in their recent financial stability report here that the shrinking buffers threaten not only borrower solvency but also the systemic stability of financial markets intertwined with CRE debt products.

Market participants must navigate the interconnectedness of these debt instruments delicately, as the calibration of risk transfer mechanisms among lenders, insurers, and investors becomes increasingly intricate. The networked dependencies formed through syndicated loan structures and tranche-level risk sharing suggest that the ripple effects of default events could be more systemic than anticipated. Consequently, the onus lies on elite fund managers to critically evaluate exposure to synthetic and securitized CRE debt, recalibrate risk assessments, and consider hedging options that account for credit spread expansions and potential liquidity crunches.

Capital Flow Adjustments and Strategic Responses by Institutional Investors

Institutional funds managing CRE portfolios are now strategically re-evaluating capital flows in light of the evolving macroeconomic landscape and associated refinancing pressures. The liquidity preference theory posits that interest rate spikes should ideally incentivize investment into higher-yielding securities; however, in the multifaceted realm of CRE, the narrative diverges. Institutional funds must now grapple with the liquidity constraints of illiquid asset holdings amidst soaring opportunity costs. The recalibration demands active portfolio optimization strategies to ensure prudent capital allocation, often necessitating a shift away from equity-rich, debt-heavy CRE positions.

As fund managers navigate these turbulent waters, a particular focus has been placed on realigning portfolio convexity while maintaining diversification. The potential for alternative investment avenues such as infrastructure assets, which offer resilient cash flows with variable rate exposure, has come to the fore. Additionally, scaling back leverage ratios and re-deploying capital into debt instruments with floating rates embedded or those with embedded options to hedge against continued rate escalations are among the considered approaches. The emphasis on counter-cyclical strategies reinforces the narrative of adaptive resilience in institutional investment frameworks.

Furthermore, the financial conduct authorities have stressed the importance of stress testing and scenario analysis as critical components in mitigating imminent default risks. The Federal Reserve emphasizes in their 2026 financial stability manual here that fund managers should enhance their focus on resilience through disciplined liquidity management and robust risk governance frameworks. Consequently, a comprehensive reevaluation of duration risk and credit quality assessments across portfolio holdings becomes imperative.

Timeliness in Market Reactions: Anticipating and Navigating Potential Contagion

The timing and accuracy of market reactions to refinancing challenges are crucial in preempting potential contagion scenarios in the CRE market. As debt maturities loom, the window for strategic pre-emptive actions narrows considerably. The capacity to forecast stress points accurately hinges on a granular understanding of market indicators, such as rental yield curves, occupancy rates, and tenant creditworthiness, which are vital for anticipating cash flow disruptions. The dichotomy between opportunistic acquisition strategies versus prudent divestitures necessitates a fine equilibrium to capitalize on distressed asset acquisitions while mitigating downside exposure.

The intricacies of market sentiment and its impact on asset re-pricing must be meticulously managed by elite fund managers. The amplifying role of media narratives and investor sentiment—amplifying or dampening market reactions—requires a deft melding of quantitative analysis with behavioral finance insights. The feedback loop inherent in such dynamics can contribute to self-fulfilling prophecies of liquidity traps within certain asset classifications, with negative sentiment precipitating forced asset sales at sub-optimal valuations. The role of institutional communication strategies thus becomes central to managing and tempering market expectations.

Finally, the resilience and timing of central bank interventions remain pivotal in averting systemic meltdowns. The latitude and timing of quantitative easing measures or alterations in reserve requirements could materially alter the landscape, underscoring the symbiotic relationship between monetary policy and market stability. Elite fund managers must foster strategic dialogues with key policy influencers, ensuring awareness and alignment on macro-prudential measures conducive to enhancing market confidence. As the unfolding scenario plays out, timely adaptations, informed by robust intelligence and strategic foresight, are essential for navigating what could be a formidable period of market recalibration.

| Criteria | Retail Approach | Institutional Overlay |

|---|---|---|

| Risk Tolerance | Usually Lower | Higher, with Structured Risk Management |

| Access to Data | Limited, Publicly Available | Extensive, Proprietary and Advanced Analytics |

| Capital Allocation | Smaller Scale, Individual Investments | Large Scale, Diversified Portfolio Investment |

| Decision-making Process | Emotional, Less Formal | Analytical, Systematic, and Model-based |

| Regulatory Compliance | Basic, Often Self-Managed | Comprehensive, Managed by Compliance Teams |

| Leverage Utilization | Prudent, Limited Use | Strategically Used, Enhancing Returns |

| Liquidity Needs | Higher, Short-term Focus | Lower, Long-term Commitments |

| Market Impact | Minimal, Individual Scale | Significant, Institutional Influences |

| Adaptability to Market Changes | Less Agile, Time-Consuming Adjustments | Highly Agile, Quick Strategic Shifts |

| Investment Horizon | Short to Medium Term | Medium to Long Term |

2 thoughts on “**The Imminent CRE Refinancing Catastrophe**”